B. Jupyter Notebook Tutorials#

B.1. Fishery Dynamics Tutorial#

Note

B.1.1. Tutorial: Sensitivity Analysis (SA) to discover factors shaping consequential dynamics#

This notebook demonstrates the application of sensitivity analysis to discover factors that shape the behavior modes of a socio-ecological system with dynamic human action.

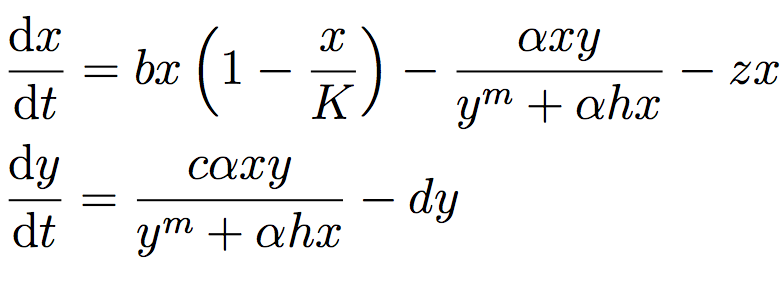

The system of differential equations below represent a system of prey (defined in the equation below as x) and predator (defined as y) fish, with a human actor harvesting the prey fish. You can read more about this system at Hadjimichael et al. (2020).

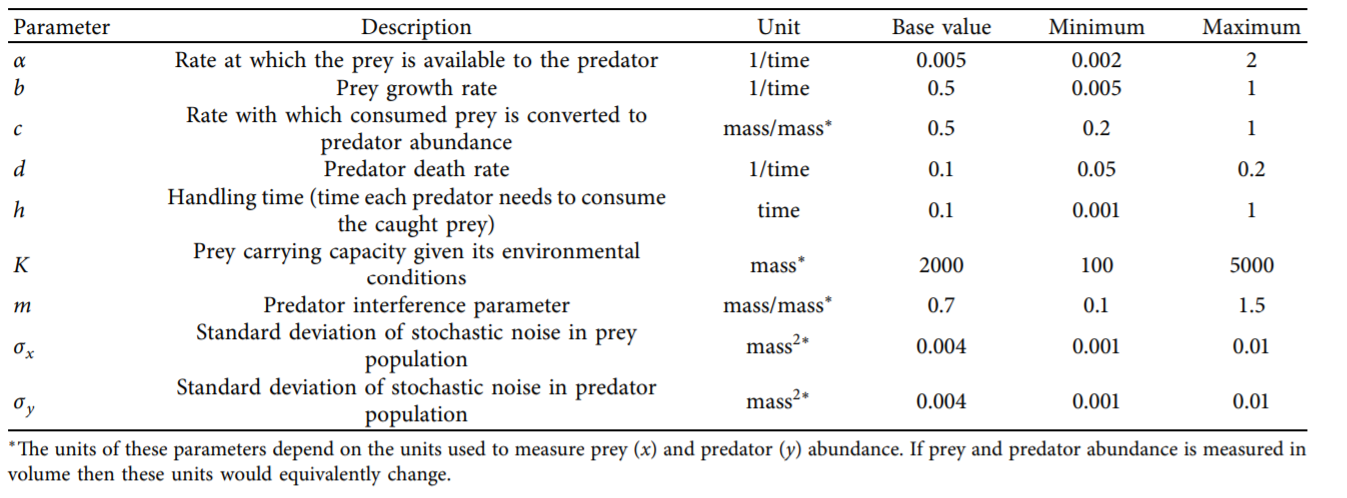

The table below defines the parameters in the system and also denotes the baseline and ranges associated with each uncertain parameter.

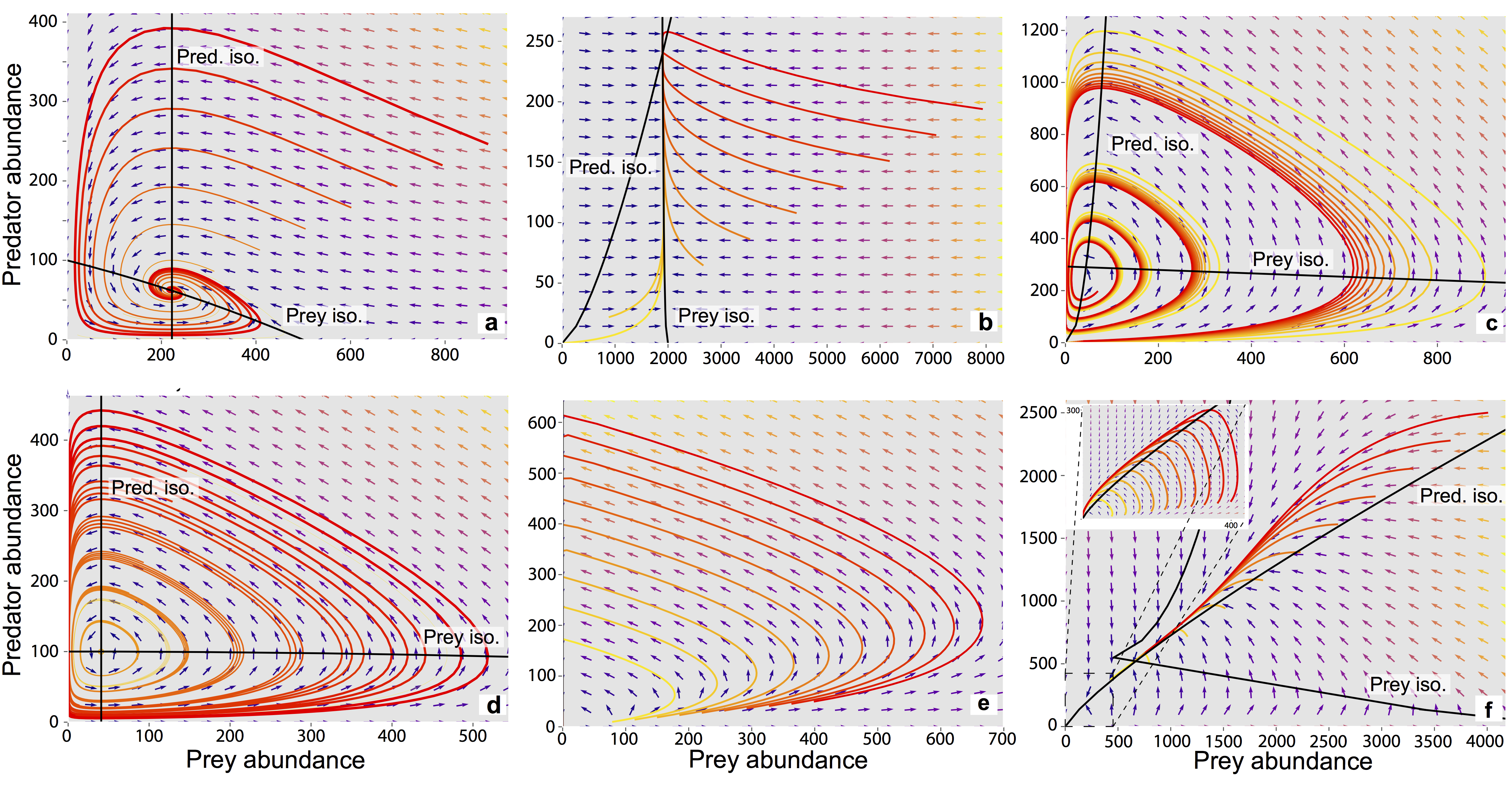

The system is simple but very rich in the dynamic behaviors it exhibits. This complexity is accompanied by the presence of several equilibria that come in and out of existence with different parameter values. The equilibria also change in their stability according to different parameter values, giving rise to different behavior modes as shown by the diverse predator and prey abundace trajectories in the figure below.

In the unharvested system (without the human actor) the stability of several of these equilibria can be derived analytically. The task becomes significantly more difficult when the adaptive human actor is introduced, deciding to harvest the system at different rates according to their objectives and preferences.

Sensitivity analysis methods can help us identify the factors that most control these dynamics by exploring the space of parameter values and seeing how system outputs change as a result.

Through previously conducted optimization, there already exists a set of potential harvesting strategies that were identified in pursuit of five objectives:

Maximize Harvesting Discounted Profits (Net Present Value)

Minimize Prey Population Deficit

Minimize Longest Duration of Consecutive Low Harvest

Maximize Worst Harvest Instance

Minimize Harvest Variance

The identified harvesting strategies also meet the necessary constraint of not causing inadvertent predator collapse.

We will be examining the effects of parametric uncertainty on these identified strategies, particularly focusing on two strategies: one selected to maximize harvesting profits and one identified through previous analysis to perform ‘well enough’ for all objectives across a wide range of states of the world (referred to as the ‘robust’ harvesting policy).

B.1.1.1. Let’s get started!#

In this tutorial, we will be loading in data that has been produced in Hadjimichael et al. (2020). Before we start our analysis, we’ll load the relevant Python libraries.

# Import necessary libraries

import msdbook

import numpy as np

import matplotlib.pyplot as plt

from SALib.sample import saltelli

from SALib.analyze import sobol

from matplotlib import patheffects as pe

# load example data

from msdbook.install_supplement import install_package_data

install_package_data()

%matplotlib inline

%config InlineBackend.print_figure_kwargs = {'bbox_inches':None}

Downloading example data for msdbook version 0.1.5...

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/uncertain_params_bounds.txt

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_metric_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_vary_delta.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_mth_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/solutions.resultfile

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/3704614_heatmap.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/LHsamples_original_1000.txt

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/3704614_pseudo_r_scores.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/param_values.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_yr_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_mth_delta.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7000550_pseudo_r_scores.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/collapse_days.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/hymod_params_256samples.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_vary_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7000550_heatmap.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7200799_heatmap.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_yr_delta.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7200799_pseudo_r_scores.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/LeafCatch.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/hymod_simulations_256samples.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/Robustness.txt

B.1.1.2. Step 1: Load identified solutions and explore performance#

Here we load in the solution set obtained in Hadjimichael et al. (2020). The solution set contains the decision variables and objectives associated with a variety of harvesting policies. For this tutorial, we focus on comparing two policies: harvesting profits and one that performs robustly across all objectives. Below, we are reading in the decision variables and objectives from an external file that can be found within the msdbook package data.

robustness = msdbook.load_robustness_data()

results = msdbook.load_profit_maximization_data()

robust_solution = np.argmax(robustness[:,-1]) #pick robust solution

profit_solution = np.argmin(results[:,6]) #pick profitable solution

objective_performance = -results[:,6:] #Retain objective values

# Get decision variables for each of the policies

highprofitpolicy = results[profit_solution,0:6]

mostrobustpolicy = results[robust_solution,0:6]

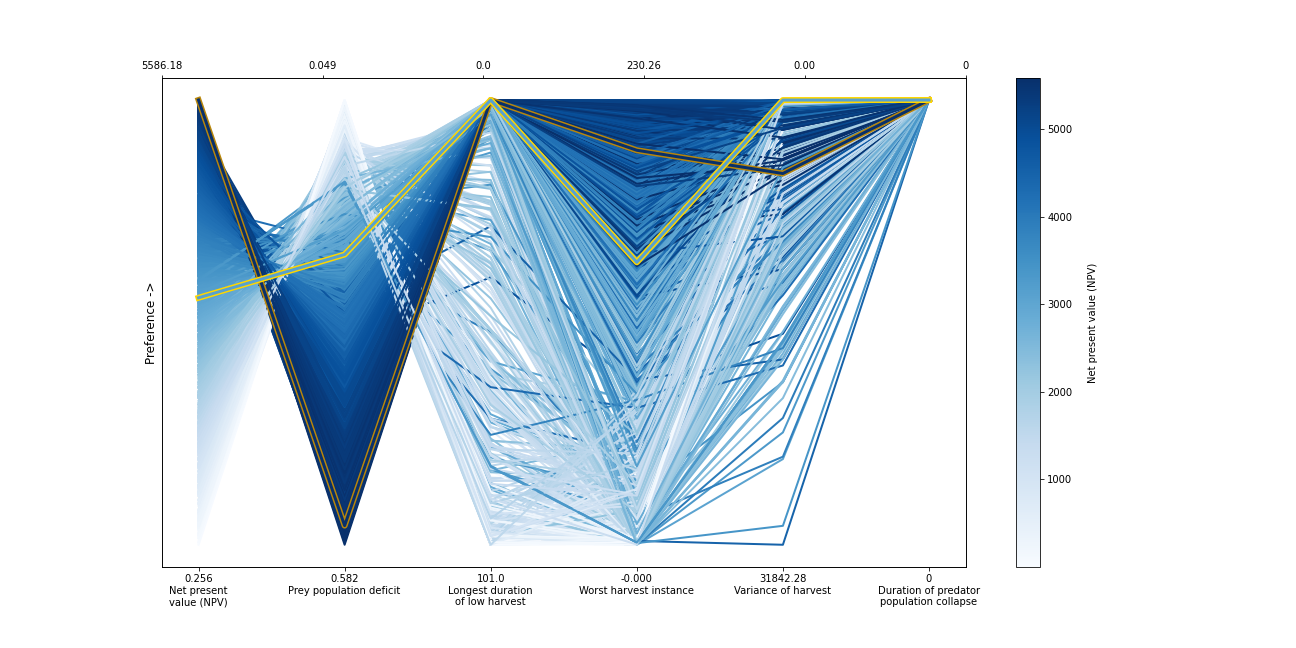

Next we plot the identified solutions with regards to their objective performance in a parallel axis plot

Tip

View the source code used to create this plot here: plot_objective_performance

ax, ax1 = msdbook.plot_objective_performance(objective_performance, profit_solution, robust_solution)

The solution set from the optimization in Hadjimichael et al. (2020) are presented in a parallel axis plot where each of the five objectives (and one constraint) are represented as an axis. Each solution on the Pareto front is represented as a line where the color of the line indicates the value of the NPV objective. The preference for objective values is in the upward direction. Therefore, the ideal solution would be a line straight across the top of the plot that satisfies every objective. However, no such line exists because there are tradeoffs when sets of objectives are prioritized over the others. When lines cross in between axes, this indicates a tradeoff between objectives (as seen in the first two axes).The solution that is most robust in the NPV objective has the highest value on the first axis and is outlined in dark gold. The solution that is most robust across all objectives is outlined in a brighter yellow. A parallel axis is an effective visual to characterize high-dimensional tradeoffs in the system and visualize differences in performance across policies.

B.1.1.3. Step 2: Use SALib to generate a sample for a Sobol sensitivity analysis#

In Step 1, we showed how the optimized harvesting policies performed in the objective space, which utilized the baseline parameters outlined in the table above. Now, we are interested in understanding how sensitive our two policies are to alternative states of the world that may be characterized by different parameter values. To do so, we first need to define the problem dictionary that allows us to generate these alternative states of the world.

# Set up SALib problem

problem = {

'num_vars': 9,

'names': ['a', 'b', 'c', 'd', 'h', 'K', 'm', 'sigmaX', 'sigmaY'],

'bounds': [[0.002, 2], [0.005, 1], [0.2, 1], [0.05, 0.2], [0.001, 1],

[100, 5000], [0.1, 1.5], [0.001, 0.01], [0.001, 0.01]]

}

Then we use the following command to generate a Saltelli sample from these defined ranges:

param_values = saltelli.sample(problem, 1024, calc_second_order=False)

Generally, it is a good idea to save the result of the sample since it is often reused and regenerating it produces a different sample set. For this reason, we will load one from file that was previously generated.

# load previously generated Saltelli sample from our msdbook package data

param_values = msdbook.load_saltelli_param_values()

B.1.1.4. Step 3: Evaluate the system over all generated states of the world#

Now we re-evaluate how well the policies do in the new states of the world. In order to characterize failure of a policy, we identify the states where the predator population collapses, as an inadvertent consequence of applying the harvesting strategy under a state of the world different from the one originally assumed. Due to how long this step takes to execute within the tutorial, we will read in the solutions from an external file. However, the block of code below shows how evaluation can be implemented.

# create array to store collapse values under both policies

collapse_days = np.zeros([len(param_values), 2])

# evaluate performance under every state

for i in range(len(param_values)):

additional_inputs = np.append(['Previous_Prey'],

[param_values[i,0],

param_values[i,1],

param_values[i,2],

param_values[i,3],

param_values[i,4],

param_values[i,5],

param_values[i,6],

param_values[i,7],

param_values[i,8]])

collapse_days[i,0]=fish_game(highprofitpolicy, additional_inputs)[1][0]

collapse_days[i,1]=fish_game(mostrobustpolicy, additional_inputs)[1][0]

# load the simulation data from our msdbook package data

collapse_days = msdbook.load_collapse_data()

B.1.1.5. Step 4: Calculate sensitivity indices#

Now we use a Sobol sensitivity analysis to calculate first-order, second-order, and total-order sensitivity indices for each parameter and for each of the two policies. These indicies help determine which factors explain the most variability in the number of days of predator population collapse.

#Perform the Sobol SA for the profit-maximizing solution

Si_profit = sobol.analyze(problem, collapse_days[:, 0],

calc_second_order=False,

conf_level=0.95,

print_to_console=True)

#Perform the Sobol SA for the robust solution

Si_robustness = sobol.analyze(problem,

collapse_days[:, 1],

calc_second_order=False,

conf_level=0.95,

print_to_console=True)

ST ST_conf

a 0.226402 0.036146

b 0.066819 0.013347

c 0.004395 0.004023

d 0.024509 0.006993

h 0.009765 0.005488

K 0.020625 0.009494

m 0.897971 0.066470

sigmaX 0.000136 0.000149

sigmaY 0.000739 0.001040

S1 S1_conf

a 0.087936 0.044236

b 0.000554 0.021474

c -0.002970 0.004590

d 0.001206 0.015881

h 0.004554 0.007998

K 0.003843 0.012661

m 0.751301 0.071862

sigmaX -0.000325 0.001245

sigmaY -0.001887 0.002768

Looking at the total-order indices, (ST) factors \(m\), \(a\), \(b\), \(d\) and \(K\) explain a non-negligible amount of variance therefore have an effect on the stability of this system. Looking at the first-order indices (S1), we also see that besides factors \(m\) and \(a\), all other factors are important in this system through their interactions, which make up the difference between their S1 and ST indices. This shows the danger of limiting sensitivity analyses to first order effects, as factor importance might be significantly misjudged.

These findings are supported by the analytical condition of equilibrium stability in this system:

In an unharvested system, this condition is both necessary and sufficient for the equilibrium of the two species coexisting to be stable.

When adaptive human action is introduced however, this condition is still necessary, but no longer sufficient, as harvesting reduces the numbers of prey fish and as a result reduces the resources for the predator fish. Since this harvesting value is not constant, but can dynamically adapt according to the harvester’s objectives, it cannot be introduced into this simple equation.

B.1.1.6. Step 5: Explore relationship between uncertain factors and performance#

In the following steps, we will use the results of our sensitivity analysis to investigate the relationships between parametric uncertainty, equilibrium stability and the performance of the two policies.

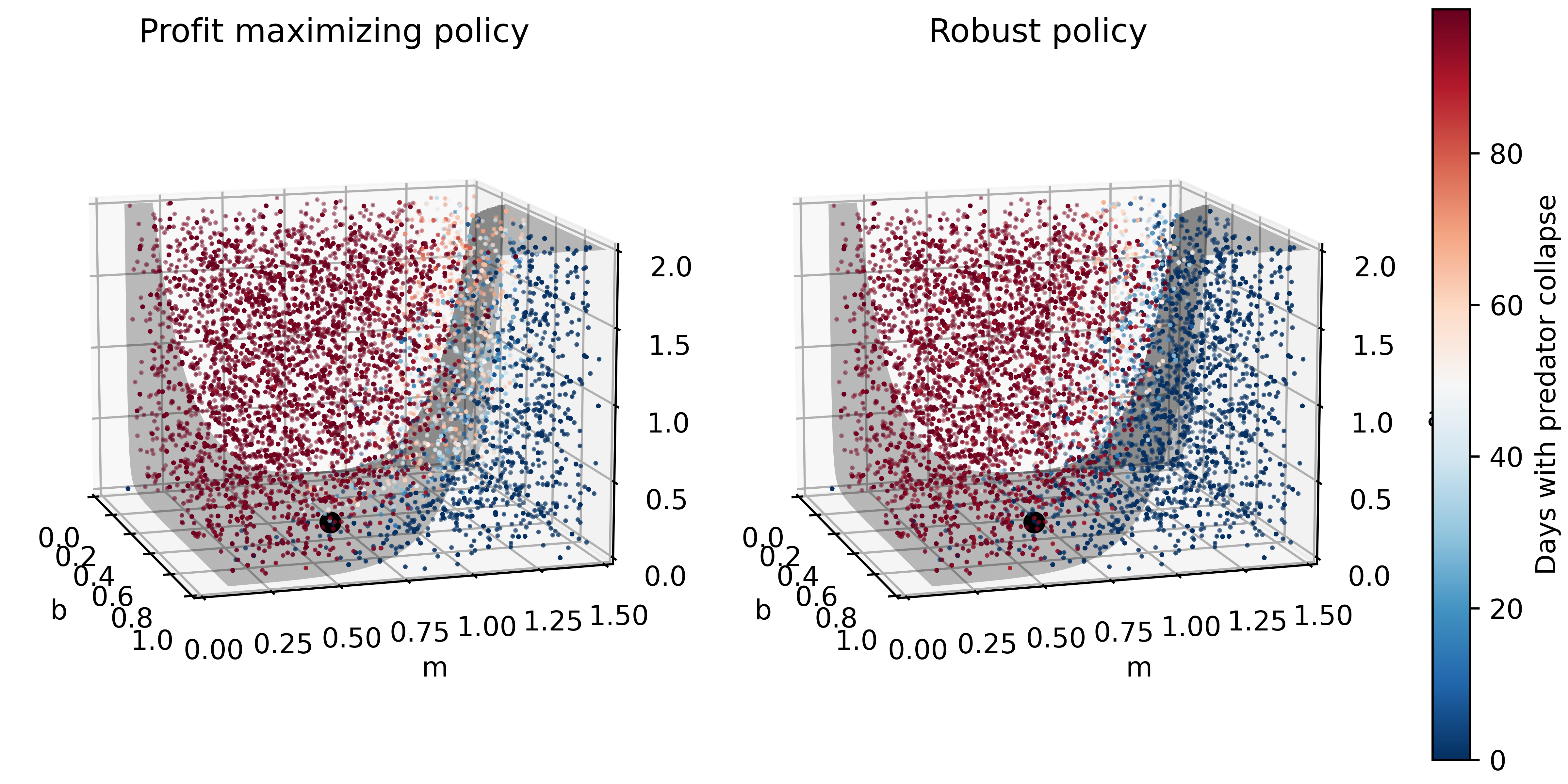

We can use the top three factors identified (\(m\), \(a\), and \(b\)) to visualize the performance of our policies in this three-dimensional parametric space.

We first define the stability condition, as a function of \(b\) and \(m\), and calculate the corresponding values of \(a\).

def inequality(b, m, h, K):

return ((b**m)/(h*K)**(1-m))

# boundary interval that separates successful and failed states of the world

b = np.linspace(start=0.005, stop=1, num=1000)

m = np.linspace(start=0.1, stop=1.5, num=1000)

h = np.linspace(start=0.001, stop=1, num=1000)

K = np.linspace(start=100, stop=2000, num=1000)

b, m = np.meshgrid(b, m)

a = inequality(b, m, h, K)

a = a.clip(0,2)

Tip

View the source code used to create this plot here: plot_factor_performance

# generate plot

ax1, ax2 = msdbook.plot_factor_performance(param_values, collapse_days, b, m, a)

These figures show the combinations of factors that lead to success or failure in different states of the world for the profit-maximizing and robust policies. Each point is a state of the world, characterized by specific values of the parameters, and ideally, we would like the color of the point to be blue, to represent that there are a low number of days with a predator collapse in that world. The gray curve denotes the highly non-linear nature of the boundary, defined by the stability condition, that separates successful and failed states of the world. The figures demonstrate the following key points:

First, as asserted above, the policies interact with the system in different and complex ways. In the presence of human action, the stability condition is not sufficient in determining whether the policy will succeed, even though it clearly shapes the system in a fundamental manner.

Secondly, the robust policy manages to avoid collapse in many more of the sampled states of the world, indicated by the number of blue points. The robust policy avoids collapse in 31% of worlds versus 14% in the profit-maximizing policy.This presents a clear tradeoff between profit-maximizing performance androbustness against uncertainty.

B.1.1.7. Tips to Apply Sobol SA and Scenario Discovery to your Problem#

In this tutorial, we demonstrated a Sobol SA to identify the most important factors driving the behavior of a system (i.e. the number of the collapse days). In order to apply this methodology to your problem, you will need to have a set of optimized policies for your system that you are interested in analyzing. The general workflow is as follows:

Choose sampling bounds for your parameters and set up the problem dictionary as in Step 2 above.

Generate samples, or alternative states of the world using the

saltelli.samplefunction.Evaluate your policies on the alternative states of the world. For your application, you will also need to develop a rule for determining success or failure of your policy in a new SOW. In this tutorial, success was denoted by a small number of collapse days. Ultimately, the rule will be specific to your application and can include various satisficing criteria.

Calculate the Sobol indices and discover the most important parameters driving success and failure.

Finally, use a similar plotting procedure as in step 5 to identify the combination of parameter values that lead to success and failure in the system.

B.2. Sobol SA Tutorial#

Note

B.2.1. Tutorial: Sensitivity Analysis (SA) using the Saltelli sampling scheme with Sobol SA#

In this tutorial, we will set up a workflow to investigate how sensitive the output of a function is to its inputs. Why might you want to do this? Imagine that this function represents a complex system, such as the rainfall-runoff process of a watershed model, and that you, the researcher, want to investigate how your choice of input parameter values are affecting the model’s characterization of runoff in the watershed. Your parameter values are likely uncertain and can take on any value in a pre-defined range. Using a Sobol SA will allow you to sample different values of your parameters and calculate how sensitive your output of interest is to certain parameters. Below, we demonstrate Sobol SA for a simple function to illustrate the method, but the workflow can be applied to your own problem of interest!

In order to conduct this analysis, we will use the popular Python Sensitivity Analysis Library (SALib) to:

Generate a problem set as a dictionary for our Ishigami function that has three inputs

Generate 2048 samples for our problem set using the Saltelli [1] [2] sampling scheme

Execute the Ishigami function for each of our samples and gather the outputs

Compute the sensitivity analysis to generate first-order and total-order sensitivity indices using the Sobol [3] method

Interpret the meaning of our results

B.2.1.1. Let’s get started!#

NOTE: Content from this tutorial is taken directly from the SALib “Basics” walkthrough.

# Import relevant libraries

import matplotlib.pyplot as plt

import SALib.sample.sobol as sobol_sample

from SALib.analyze import sobol

from SALib.test_functions import Ishigami

B.2.1.2. Step 1: Generate the problem dictionary#

The Ishigami function is of the form:

The function has three inputs, 𝑥1, 𝑥2, 𝑥3 where 𝑥𝑖 ∈ [−𝜋, 𝜋]. The constants \(a\) and \(b\) are defined as 7.0 and 0.1 respectively.

#Create a problem dictionary. Here we supply the number of variables, the names of each variable, and the bounds of the variables.

problem = {

'num_vars': 3,

'names': ['x1', 'x2', 'x3'],

'bounds': [[-3.14159265359, 3.14159265359],

[-3.14159265359, 3.14159265359],

[-3.14159265359, 3.14159265359]]

}

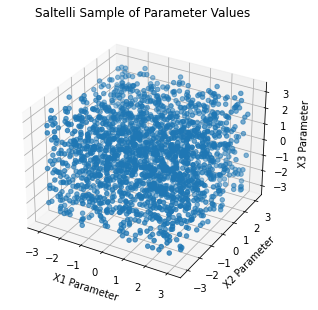

B.2.1.3. Step 2: Generate samples using the Saltelli sampling scheme#

Sobol SA requires the use of the Saltelli sampling scheme. The output of

the saltelli.sample function is a NumPy array that is of shape 2048

by 3. The sampler generates 𝑁∗(2𝐷+2) samples, where in this example, N

is 256 (the argument we supplied) and D is 3 (the number of model

inputs), yielding 2048 samples. The keyword argument

calc_second_order=False will exclude second-order indices, resulting

in a smaller sample matrix with 𝑁∗(𝐷+2) rows instead. Below, we plot the

resulting Saltelli sample.

# Generate parmeter values using the saltelli.sample function

param_values = sobol_sample.sample(problem, 256)

print(f"`param_values` shape: {param_values.shape}")

param_values shape: (2048, 3)

# Plot the 2048 samples of the parameters

fig = plt.figure(figsize = (7, 5))

ax = plt.axes(projection ="3d")

ax.scatter3D(param_values[:,0], param_values[:,1], param_values[:,2])

ax.set_xlabel('X1 Parameter')

ax.set_ylabel('X2 Parameter')

ax.set_zlabel('X3 Parameter')

plt.title("Saltelli Sample of Parameter Values")

plt.show()

B.2.1.4. Step 3: Execute the Ishigami function over our sample set#

SALib provides a nice wrapper to the Ishigami function that allows the

user to directly pass the param_values array we just generated into

the function directly.

Y = Ishigami.evaluate(param_values)

B.2.1.5. Step 4: Compute first-, second-, and total-order sensitivity indices using the Sobol method#

The sobol.analyze function will use our problem dictionary and the

result of the Ishigami runs (Y) to compute first-, second-, and

total-order indicies.

Si = sobol.analyze(problem, Y)

Si is a Python dict with the keys “S1”, “S2”, “ST”, “S1_conf”,

“S2_conf”, and “ST_conf”. The _conf keys store the corresponding

confidence intervals, typically with a confidence level of 95%. Use the

keyword argument print_to_console=True to print all indices. Or, we

can print the individual values from Si as shown in the next step.

B.2.1.6. Step 5: Interpret our results#

We execute the following code and take a look at our first-order indices

(S1) for each of our three inputs. These indicies can be interpreted

as the fraction of variance in the output that is explained by each

input individually.

first_order = Si['S1']

print('First-order:')

print(f"x1: {first_order[0]}, x2: {first_order[1]}, x3: {first_order[2]}")

First-order:

x1: 0.3184242969763115, x2: 0.4303808201623416, x3: 0.022687722804980225

If we were to rank the importance of the inputs in how much they individually explain the variance in the output, we would rank them from greatest to least importance as follows: 𝑥2, 𝑥1 and then 𝑥3. Since 𝑥3 only explains 2% of the output variance, it does not explain output variability meaningfully. Thus, this indicates that there is contribution to the output variance by 𝑥2 and 𝑥1 independently, whereas 𝑥3 does not contribute to the output variance. Determining what inputs are most important or what index value is meaningful is a common question, but one for which there is no general rule or threshold. This question is problem and context-dependent, but procedures have been identified to rank order influential inputs and which can be used to identify the least influential factors. These factors can be fixed to simplify the model [4] [5] [6].

Next, we evaluate the total-order indices, which measure the contribution to the output variance caused by varying the model input, including both its first-order effects (the input varying alone) and all higher-order interactions across the input parameters.

total_order = Si['ST']

print('Total-order:')

print(f"x1: {total_order[0]}, x2: {total_order[1]}, x3: {total_order[2]}")

Total-order:

x1: 0.5184119098161343, x2: 0.41021260250026054, x3: 0.2299058431439953

The magnitude of the total order indices are substantially larger than the first-order indices, which reveals that higher-order interactions are occurring, i.e. that the interactions across inputs are also explaining some of the total variance in the output. Note that 𝑥3 has non-negligible total-order indices, which indicates that it is not a consequential parameter when considered in isolation, but becomes consequential and explains 25% of variance in the output through its interactions with 𝑥1 and 𝑥2.

Finally, we can investigate these higher order interactions by viewing the second-order indices. The second-order indicies measure the contribution to the output variance caused by the interaction between any two model inputs. Some computing error can appear in these sensitivity indices, such as negative values. Typically, these computing errors shrink as the number of samples increases.

second_order = Si['S2']

print("Second-order:")

print(f"x1-x2: {second_order[0,1]}")

print(f"x1-x3: {second_order[0,2]}")

print(f"x2-x3: {second_order[1,2]}")

Second-order:

x1-x2: -0.043237389723234154

x1-x3: 0.17506452088709862

x2-x3: -0.03430682392607577

We can see that there are strong interactions between 𝑥1 and 𝑥3. Note that in the Ishigami function, these two variables are multiplied in the last term of the function, which leads to interactive effects. If we were considering first order indices alone, we would erroneously assume that 𝑥3 explains no variance in the output, but the second-order and total order indices reveal that this is not the case. It’s easy to understand where we might see interactive effects in the case of the simple Ishigami function. However, it’s important to remember that in more complex systems, there may be many higher-order interactions that are not apparent, but could be extremely consequential in explaining the variance of the output.

B.2.1.7. Tips to Apply Sobol SA to Your Own Problem#

In this tutorial, we demonstrated how to apply an SA analysis to a simple mathematical test function. In order to apply a Sobol SA to your own problem, you will follow the same general workflow that we defined above. You will need to:

Choose sampling bounds for your parameters and set up the problem dictionary as in Step 1 above.

Generate samples using the

saltelli.samplefunction. This step is problem-dependent and note that the Sobol method can be computationally intensive depending on the model being analyzed. For example, for a simple rainfall-runoff model such as HYMOD, it has been recommended to run a sample size of at least N = 10,000 (which translates to 60,000 model runs). More complex models will be slower to run and will also require more samples to calculate accurate estimates of Sobol indices. Once you complete this process, pay attention to the confidence bounds on your sensitivity indices to see whether you need to run more samples.Run the parameter sets through your model. In the example above, the Ishigami function could be evaluated through SALib since it is a built in function. For your application, you will need to run these parameter sets through the problem externally and save the output. The output file should contain one row of output values for each model run.

Calculate the Sobol indices. Now, the Y will be a numpy array with your external model output and you will need to include the parameter samples as an additional argument.

Finally, we interpet the results. If the confidence intervals of your dominant indices are larger than roughly 10% of the value itself, you may want to consider increasing your sample size as computation permits. You should additionally read the references noted in Step 5 above to understand more about identifying important factors.

References

B.3. Logistic Regression Tutorial#

Note

B.3.1. Tutorial: Logistic Regression for Factor Mapping#

This tutorial replicates a scenario discovery analysis performed in Hadjimichael et al. (2020).

B.3.1.1. Background#

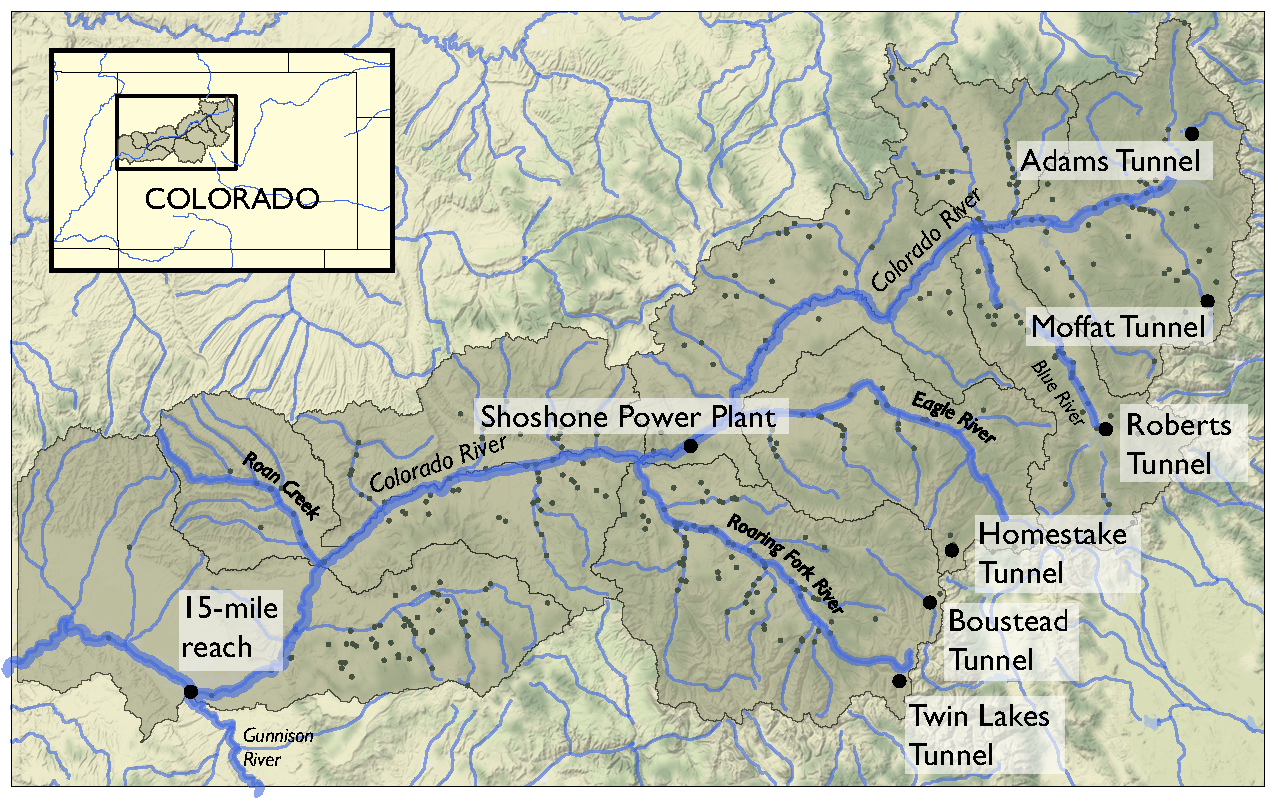

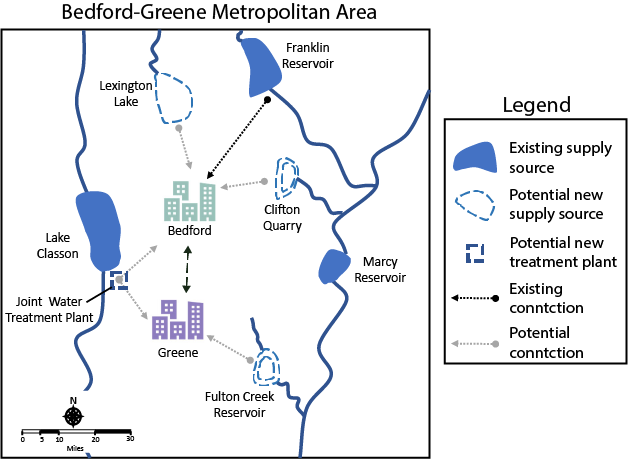

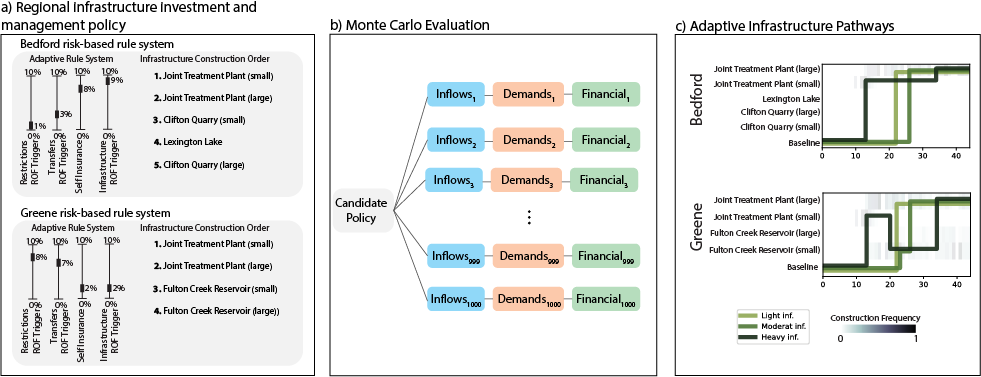

Planners in the the Upper Colorado River Basin (UCRB, shown in the figure below) are seeking to understand the vulnerability of water users to uncertainties stemming from climate change, population growth and water policy changes. The UCRB spans 25,682 km2 in western Colorado and is home to approximately 300,000 residents and 1,012 km2 of irrigated land. Several thousand irrigation ditches divert water from the main river and its tributaties for irrigation (shown as small black dots in the figure). Transmountain diversions of approximately 567,400,000 m3 per year are exported for irrigation, industrial and municipal uses in northern and eastern Colorado, serving the major population centers of Denver and Colorado Springs. These diversions are carried through tunnels, shown as large black dots in the figure.

An important planning consideration is the water rights of each user, defined by seniority across all water uses (irrigation diversions, transboundary diversions, power plants etc.) in the basin. To assess the vulnerability of users with varying degrees of water rights seniority, planners simulate the system across an ensemble of scenarios using the state of Colorado’s StateMod platform. The model simulates streamflow, diversions, instream demands, and reservoir operations.

Hadjimichael et al. (2020) employ an exploratory analysis by simulating a large ensemble of plausible scenarios using StateMod and then identifying consequential decision-relevant combinations of uncertain factors, termed scenario discovery. Focusing on decision-relevant metrics (metrics that are important to the user, the scenario discovery is applied to the water shortages experienced by each individual user (i.e., not on a single basin-wide or sector-wide metric). For this training example, we’ll be performing scenario discovery for three different water users: two irrigation users and one municipal user.

B.3.1.2. Let’s get started!#

In this tutorial, we will be loading in data that has been produced in Hadjimichael et al. (2020). Before we start our analysis, we’ll load the relevant Python libraries, example data, and information for the three users.

# Import libraries

import numpy as np

import pandas as pd

import matplotlib as mpl

import matplotlib.pyplot as plt

from msdbook.package_data import load_basin_param_bounds, load_lhs_basin_sample, load_user_heatmap_array, load_user_pseudo_scores

from msdbook.utils import fit_logit, plot_contour_map

# Select the IDs for the three users that we will perform the analysis for

all_IDs = ['7000550','7200799','3704614']

usernames = ['Medium seniority irrigation',

'Low seniority irrigation',

'Transbasin municipal diversion']

nStructures = len(all_IDs)

# Install package data

from msdbook.install_supplement import install_package_data

install_package_data()

Downloading example data for msdbook version 0.1.5...

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/uncertain_params_bounds.txt

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_metric_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_vary_delta.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_mth_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/solutions.resultfile

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/3704614_heatmap.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/LHsamples_original_1000.txt

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/3704614_pseudo_r_scores.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/param_values.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_yr_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_mth_delta.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7000550_pseudo_r_scores.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/collapse_days.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/hymod_params_256samples.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_vary_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7000550_heatmap.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7200799_heatmap.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_yr_delta.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7200799_pseudo_r_scores.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/LeafCatch.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/hymod_simulations_256samples.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/Robustness.txt

B.3.1.3. Step 1: Load Latin hypercube sample and set up problem#

To examine regional vulnerability, we generate an ensemble of plausible

future states of the world (SOWs) using Latin Hypercube Sampling. For

this tutorial, we’ll load a file containing 1,000 samples across 14

parameters. The sampled parameters encompass plausible changes to the

future state of the basin, including changes to hydrology, water demands

(irrigation, municipal & industry, transbasin), and institutional and

environmental factors (environmental flows, reservoir storage, operation

of the Shoshone Power Plant). These samples are taken from ranges

identified in param_bounds. Below we load in the 1000 samples, the

range of values that the samples can take for each parameter, and the

parameter names. More information on what each parameter constitutes can

be found in Table 1 of Hadjimichael et al., 2020.

# Identify the bounds for each of the 14 parameters

param_bounds = msdbook.load_basin_param_bounds()

#Load in the parameter samples

LHsamples = msdbook.load_lhs_basin_sample()

#Create an array of the parameter names

param_names=['Irrigation demand multiplier','Reservoir loss','Transbasin demand multiplier',

'Municipal & industrial multiplier', 'Shoshone','Environmental flows',

'Evaporation change','Mean dry flow','Dry flow variance',

'Mean wet flow','Wet flow variance','Dry-dry probability',

'Wet-wet probability', 'Snowmelt shift']

B.3.1.4. Step 2: Define decision-relevant metrics for illustration#

Scenario discovery attempts to identify parametric regions that lead to ‘success’ and ‘failure’. For this demonstration we’ll be defining ‘success’ as states of the world where a shortage level doesn’t exceed its historical frequency.

B.3.1.5. Step 3: Run the logistic regression#

Logistic regression estimates the probability that a future SOW will be classified as a success or failure given a set of performance criteria. A logistic regression model is defined by:

where \(p_i\) is the probability the performance in the \(i^{th}\) SOW will be classified as a success, \(X_i\) is the vector of covariates describing the \(i^{th}\) SOW, and \(\beta\) is the vector of coefficients describing the relationship between the covariates and the response, which here will be estimated using maximum likelihood estimation.

A logistic regression model was fit to the ensemble of SOWs using the performance criteria defined in step 2. Logistic regression modeling was conducted using the Statsmodel Python package. The data required for the full analysis is too large to include in this tutorial, but results can be found in the data file loaded below.

The results files contain the occurrence of different shortage frequency and magnitude combinations under the experiment, in increments of 10, between 0 and 100. These combinations (100 for each user) are alternative decision-relevant metrics that can be used for scenario discovery.

# Set arrays for shortage frequencies and magnitudes

frequencies = np.arange(10, 110, 10)

magnitudes = np.arange(10, 110, 10)

realizations = 10

# Load performance and pseudo r scores for each of the users

results = [msdbook.load_user_heatmap_array(all_IDs[i]) / 100 for i in range(len(all_IDs))]

B.3.1.6. Step 4: Factor ranking#

To rank the importance of each uncertain factor, we utilize McFadden’s psuedo-R2, a measure that quantifies the improvement of the model when utilizing each given predictor as compared to prediction using the mean of the data set:

Here \(ln \hat{L}(M_{full})\) is the log likelihood of the full model (including the predictor) and \(ln \hat{L}(M_{intercept})\) is the log likelihood of the intercept model (which predicts the mean probability of success across all SOWs).

Higher values of McFadden’s pseudo-R2 indicate higher factor importance (when the likelihood of the full model approaches one, the ratio of the likelihood of the full model compared to the intercept model will get very small).

# Load the pseudo-R^2 scores

scores = [msdbook.load_user_pseudo_scores(all_IDs[i]) for i in range(len(all_IDs))]

# Select indices of frequency and magnitudes that will be used for the visualization

freq = [1,0,0]

mag = [7,3,7]

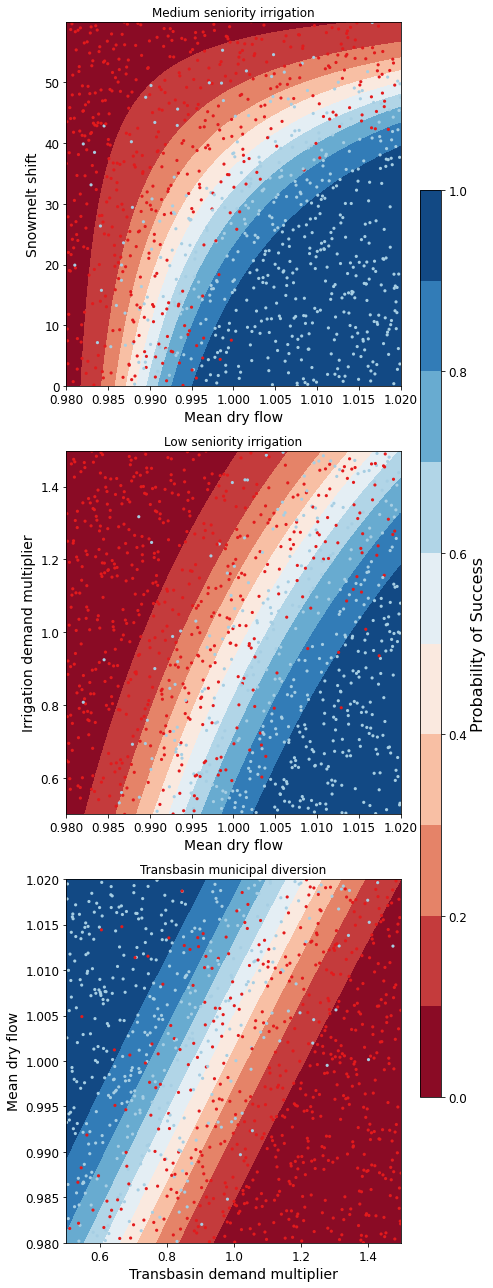

B.3.1.7. Step 5: Draw factor maps#

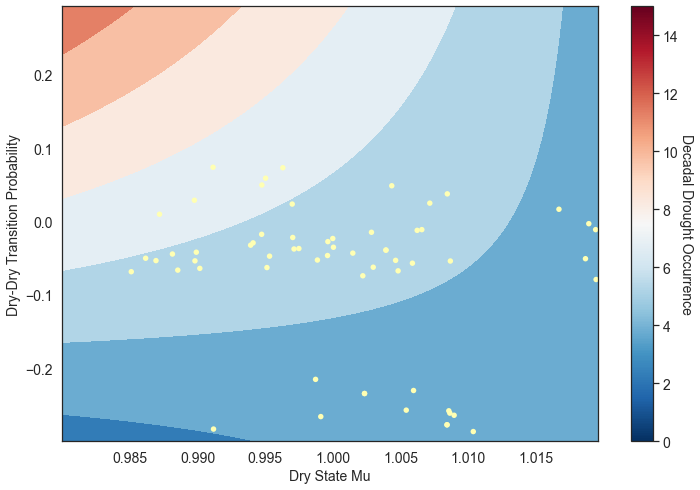

The McFadden’s pseudo-R2 scores files contain preliminary logistic regression results on parameter importance for each of these combinations. Using these pseudo-R2 scores we will identify the two most important factors for each metric which we’ll use to generate the final scenario discovery maps (note: there may be more than two important metrics for each user, but here we will demonstrate by mapping two).

# setup figure

fig, axes = plt.subplots(3,1, figsize=(6,18), tight_layout=True)

fig.patch.set_facecolor('white')

for i in range(len(axes.flat)):

ax = axes.flat[i]

allSOWsperformance = results[i]

all_pseudo_r_scores = scores[i]

# construct dataframe

dta = pd.DataFrame(data=np.repeat(LHsamples, realizations, axis = 0), columns=param_names)

dta['Success'] = allSOWsperformance[freq[i],mag[i],:]

pseudo_r_scores = all_pseudo_r_scores[str(frequencies[freq[i]])+'yrs_'+str(magnitudes[mag[i]])+'prc'].values

top_predictors = np.argsort(pseudo_r_scores)[::-1][:2] #Sort scores and pick top 2 predictors

# define color map for dots representing SOWs in which the policy

# succeeds (light blue) and fails (dark red)

dot_cmap = mpl.colors.ListedColormap(np.array([[227,26,28],[166,206,227]])/255.0)

# define color map for probability contours

contour_cmap = mpl.colormaps.get_cmap('RdBu')

# define probability contours

contour_levels = np.arange(0.0, 1.05,0.1)

# define base values of the predictors

SOW_values = np.array([1,1,1,1,0,0,1,1,1,1,1,0,0,0]) # default parameter values for base SOW

base = SOW_values[top_predictors]

ranges = param_bounds[top_predictors]

# define grid of x (1st predictor), and y (2nd predictor) dimensions

# to plot contour map over

xgrid = np.arange(param_bounds[top_predictors[0]][0],

param_bounds[top_predictors[0]][1], np.around((ranges[0][1]-ranges[0][0])/500,decimals=4))

ygrid = np.arange(param_bounds[top_predictors[1]][0],

param_bounds[top_predictors[1]][1], np.around((ranges[1][1]-ranges[1][0])/500,decimals=4))

all_predictors = [ dta.columns.tolist()[i] for i in top_predictors]

dta['Interaction'] = dta[all_predictors[0]]*dta[all_predictors[1]]

# logistic regression here

predictor_list = [all_predictors[i] for i in [0,1]]

result = msdbook.fit_logit(dta, predictor_list)

# plot contour map

contourset = msdbook.plot_contour_map(ax, result, dta, contour_cmap,

dot_cmap, contour_levels, xgrid,

ygrid, all_predictors[0], all_predictors[1], base)

ax.set_title(usernames[i])

# set up colorbar

cbar_ax = fig.add_axes([0.98, 0.15, 0.05, 0.7])

cbar = fig.colorbar(contourset, cax=cbar_ax)

cbar_ax.set_ylabel('Probability of Success', fontsize=16)

cbar_ax.tick_params(axis='y', which='major', labelsize=12)

/srv/conda/envs/notebook/lib/python3.7/site-packages/statsmodels/base/model.py:127: ValueWarning: unknown kwargs ['disp']

warnings.warn(msg, ValueWarning)

Optimization terminated successfully.

Current function value: 0.378619

Iterations 8

Optimization terminated successfully.

Current function value: 0.397285

Iterations 8

Optimization terminated successfully.

Current function value: 0.377323

Iterations 8

The figure above demonstrates how different combinations of the uncertain factors lead to success or failure in different states of the world, which are denoted by the blue and red dots respectively. The probability of success and failure are further denoted by the contours in the figure. Several insights can be drawn from this figure.

First, using metrics chosen to be decision-relevant (specific to each user) causes different factors to be identified as most important by this scenario-discovery exercise (the x- and y-axes for each of the subplots). In other words, depending on what the decision makers of this system want to prioritize they might choose to monitor different uncertain factors to track performance.

Second, in the top panel, the two identified factors appear to also have an interactive effect on the metric used (shortages of a certain level and frequency in this example). In terms of scenario discovery, the Patient Rule Induction Method (PRIM) or Classification And Regression Trees (CART) would not be able to delineate this non-linear space and would therefore misclassify parameter combinations as ‘desirable’ when they were in fact undesirable, and vice versa.

Lastly, logistic regression also produces contours of probability of success, i.e. different factor-value combinations are assigned different probabilities that a shortage level will be exceeded. This allows the decision makers to evaluate these insights while considering their risk aversion.

B.3.1.8. Tips to Apply Scenario Discovery to Your Own Problem#

In this tutorial, we demonstrated how to perform a scenario discovery analysis for three different users in the UCRB. The analysis allowed us to determine which parameters the users would be most affected by and to visualize how different ranges of these parameters lead to success and failure for different users. This framework can be applicable to any other application where it is of interest to characterize success and failure based on uncertain parameter ranges. In order to apply the same framework to your own problem:

Choose sampling bounds for your parameters of interest, which will represent uncertainties that characterize your system.

Generate samples for these parameters (this can be done using the

saltelli.samplefunction or externally).Define what constitutes success and failure in your problem. In this tutorial, success was defined based on not surpassing the historical drought frequency. Choose a metric that is relevant to your problem and decision-makers that might be involved. If your model involves an optimization, you can also define metrics based on meeting certain values of these objectives.

Run the parameter sets through your model and calculate success and failure based on your metrics and across different users if applicable. This step will allow you to create the scatter plot part of the final figure.

If it is of interest, the contours on the figure can be created by fitting the logistic regression model in a similar manner as denoted in Steps 3 and 5 of the tutorial.

B.4. HYMOD Dynamics Tutorial#

Note

B.4.1. Tutorial: Sensitivity Analysis of the HYMOD Model#

The purpose of this tutorial is to demonstrate the global sensitivity analysis concepts and tools established in the Section 3.1 of the main text of this eBook. This demonstration will highlight the central role of design of experiments (Section 3.3), when implementing global sensitivity analysis tools described in Section 3.4.

We’ll explore these tools and concepts using the HYdrological MODel (HYMOD), a rainfall-runoff model developed and used for river flow forecasting. HYMOD was chosen for demonstration because its purpose is to abstract highly complex and non-linear systems. The methods demonstrated in this tutorial can be applied to numerical models that simulate other complex non-linear systems.

This tutorial will first introduce HYMOD and use it to simulate streamflows in a river basin. Next, we’ll employ sensitivity analysis concepts described in Section 3 of the main text to examine how values of HYMOD’s parameters impact streamflow predictions. Finally, we’ll explore how the effects of these parameters may change over time using time-varying sensitivity analysis.

The tutorial includes the following steps:

1.1 - Introduction to a simple hydrologic model (HYMOD)

1.2 - Input Data

1.3 - Running a basic simulation

1.4 - Model outputs

2.1 - Design of Experiments

2.2 - Sensitivity analysis for one output

2.3 - Sensitivity analysis across multiple outputs

2.4 - Time-varying sensitivity analysis

B.4.2. 1 - Introduction to HYMOD#

1.1 Overview

HYMOD is a hydrologic model (rainfall-runoff model) that simulates key hydrologic fluxes such as infiltration, streamflow and evapotranspiration. The model was originally developed and used for river flow forecasting, but it has also been been used to explore different sensitivity analysis (e.g., Herman et al., 2013), uncertainty quantification (e.g., Smith et al., 2008), and optimization (e.g., Ye et al., 2014) concepts.

HYMOD accepts two inputs - daily precipitation and daily potential evapotranspiration (PET)- and generates predictons of daily streamflow. HYMOD abstracts the highly non-linear process of runoff routing by dividing the flow into two components: quick flow, representing precipitation that quickly runs off the surface of the watershed into the stream, and slow flow, that moves through the soil and takes much longer to arrive at the stream.

To generate streamflow predictions, HYMOD first models vertical processes within the watershed to determine how much water infiltrates and evaporates from the soil at a given time step. It then determines how much water should be partitioned into quick flow and slow flow processes. Within each process it abstracts residence time (the time it takes a unit volume of water to move through the watershed and into the stream) using a series of “reservoirs” each with a calibrated residence time.

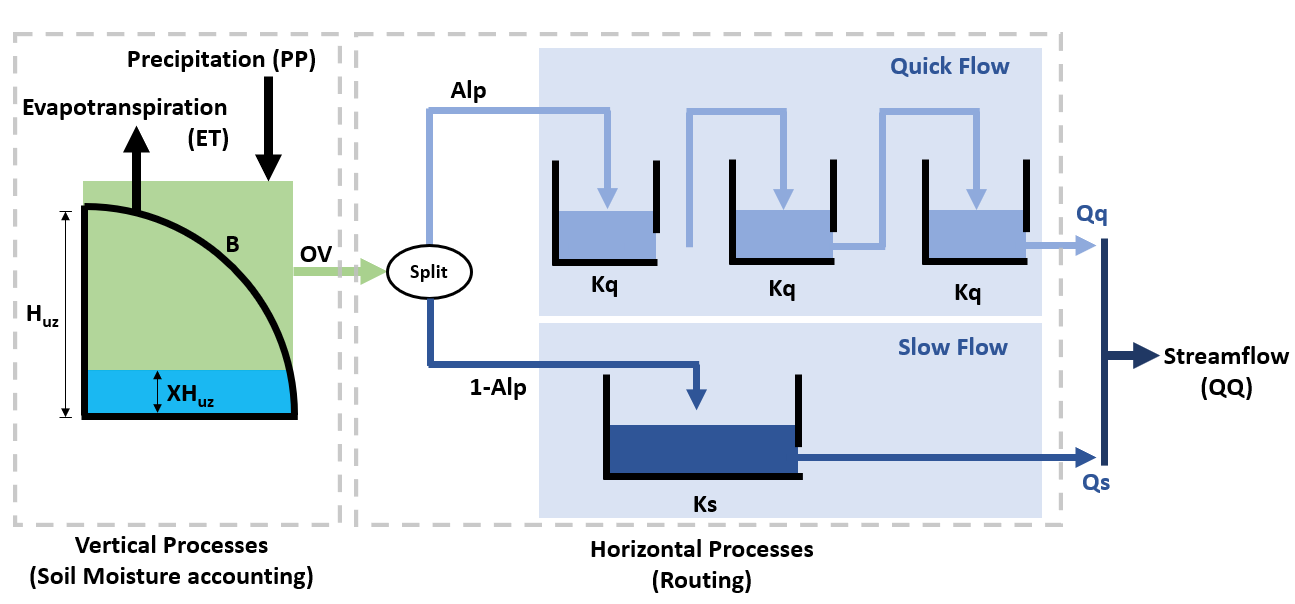

HYMOD’s representation of hydrologic processes are shown Figure 1 below and controlled by the following parameters:

\(H_{uz}\): the maximum water storage capacity of the soil (mm)

\(B_{exp}\): parameters describing the degree of spatial variability within the basin between 0 and Huz

\(Alp\): Fraction of runoff contributing to quick flow

\(K_q\): Quick flow residence time of linear infinite reservoir (the Kq values of all three linear reservoirs are the same)

\(K_s\): Slow flow residence time of linear infinite reservoir

HYMOD models the fraction of water that is stored in the soil \((F(XH_{uz}))\) using the following relationship:

where \(XH_{uz}\) is the water storage capacity of the soil; \(H_{uz}\) is the parameter describing basin maximum water storage capacity (mm); and \(B\) is the parameter describing the degree of spatial variability within the basin.

The portion of precipitation that exceeds the water storage capacity is treated as runoff.

To route runoff to streamflow, the excess runoff from the vertical processes is split into quick flow and slow flow. The proportion of runoff partitioned into quick flow and slow flow is determined by a parameter \(Alp\), which ranges between 0 and 1. Quick flow is routed through \(N\) identical quick flow tanks \(Q1, Q2... QN\) (shown above as \(N=3\)). The rate at which runoff moves through the quick flow system is described by the residence time of the quick flow tanks, \(Kq\) (day). Slow flow is routed through a parallel slow flow tank and the rate at which slow flow is routed is described by the slow flow residences time, \(Ks\) (day).

Citation: Wagener, T., Boyle, D. P., Lees, M. J., Wheater, H. S., Gupta, H. V., & Sorooshian, S. (2001). A framework for development and application of hydrological models. Hydrology and Earth System Sciences, 5(1), 13-26.

1.2 Input data

The HYMOD model only requires precipitation and potential evapotranspiration as inputs. For this example, we’ll run HYMOD using data from the Leaf River, a humid catchment located north of Collins Mississippi that has been widely used to explore HYMOD. The dataset also includes daily observed runoff that we later use to evaluate the performance of each sensitivity analysis sample set.

In the following section of code, we’ll load the necessary python libraries and read in the input file. For this exercise we’ll only use the first eleven years of data. The first five rows of the input dataset are printed to show what they look like:

import itertools

import math

import msdbook

import numpy as np

import pandas as pd

import seaborn as sns

import warnings

from matplotlib import pyplot as plt

import msdbook.hymod

from msdbook.package_data import load_hymod_input_file, load_hymod_params, load_hymod_simulation, load_hymod_monthly_simulations, load_hymod_annual_simulations, load_hymod_varying_simulations

from SALib.analyze import sobol

from sklearn import metrics

# load example data

from msdbook.install_supplement import install_package_data

install_package_data()

# load the Leaf River HYMOD input file

leaf_data = msdbook.load_hymod_input_file()

# extract the first eleven years of data

leaf_data = leaf_data.iloc[0:4015].copy()

print('Leaf River Data structure:')

# There are only three columns in the file including precipitation, potential evapotranspiration and streamflow

leaf_data.head()

Downloading example data for msdbook version 0.1.5...

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/uncertain_params_bounds.txt

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_metric_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_vary_delta.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_mth_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/solutions.resultfile

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/3704614_heatmap.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/LHsamples_original_1000.txt

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/3704614_pseudo_r_scores.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/param_values.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_yr_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_mth_delta.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7000550_pseudo_r_scores.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/collapse_days.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/hymod_params_256samples.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_vary_s1.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7000550_heatmap.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7200799_heatmap.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/sa_by_yr_delta.npy

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/7200799_pseudo_r_scores.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/LeafCatch.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/hymod_simulations_256samples.csv

Unzipped: /srv/conda/envs/notebook/lib/python3.7/site-packages/msdbook/data/Robustness.txt

Leaf River Data structure:

| Precip | Pot_ET | Strmflw | |

|---|---|---|---|

| 0 | 0.0 | 4.60 | 0.29 |

| 1 | 0.0 | 4.31 | 0.24 |

| 2 | 0.0 | 4.33 | 0.21 |

| 3 | 0.0 | 4.78 | 0.19 |

| 4 | 0.0 | 2.91 | 0.18 |

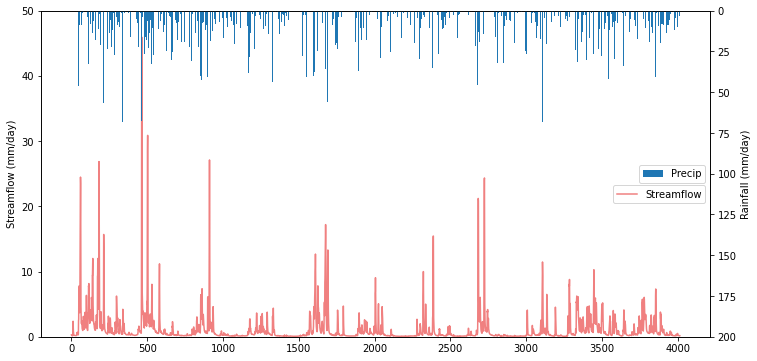

To visualize catchment hydrology, streamflow and precipitation data are usually plotted together as a combined hydrograph (streamflow ) and hyetograph (rainfall, from Greek hyetos, “rain”). Streamflow is plotted as a time series, while rainfall is shown as an inverted bar plot along the top of the graph. Streamflow labels are shown on the left y-axis, while rainfall labels are shown on the right y-axis.

# make an axis for the hydrograph

fig, strmflw_ax = plt.subplots(figsize=[12,6])

strmflw_ax.set_ylim([0, 50])

#make a second y-axis for the hyetograph

precip_ax = strmflw_ax.twinx()

precip_ax.set_ylim([0, 200])

precip_ax.invert_yaxis()

precip = leaf_data['Precip']

strmflw_ax.plot(range(0, len(leaf_data['Precip'])), leaf_data['Strmflw'], color='lightcoral')

strmflw_ax.set_ylabel('Streamflow (mm/day)')

precip_ax.bar(range(0, len(leaf_data['Precip'])), leaf_data['Precip'], width=2)

precip_ax.set_ylabel('Rainfall (mm/day)')

precip_ax.legend(['Precip'], loc='center right')

strmflw_ax.legend(['Streamflow'],bbox_to_anchor=(1, 0.48))

<matplotlib.legend.Legend at 0x7f53b95c6850>

1.3 Running a Baseline Model Simulation

We’ll start our experiment by running HYMOD using its default parameters.

# assign input parameters to generate a baseline simulated streamflow

Nq = 3 # Number of quickflow routing tanks

Kq = 0.5 # Quickflow routing tanks' rate parameter

Ks = 0.001 # Slowflow routing tank's rate parameter

Alp = 0.5 # Quick/slow split parameter

Huz = 100 # Maximum height of soil moisture accounting tank

B = 1.0 # Scaled distribution function shape parameter

# Note that the number of years is 11. One year of model warm-up and ten years are used for actual simulation

model = msdbook.hymod.hymod(Nq, Kq, Ks, Alp, Huz, B, leaf_data, ndays=4015)

1.4 Model Outputs

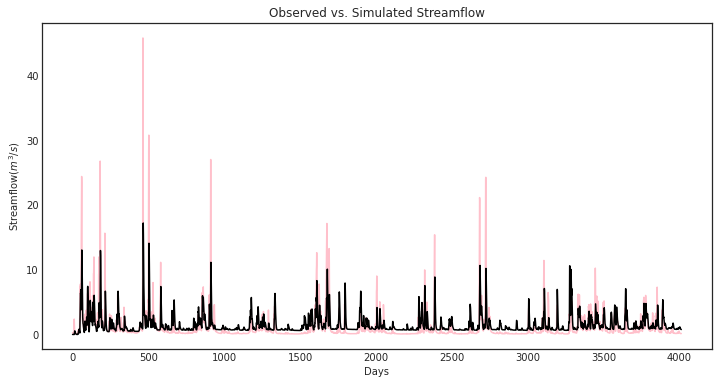

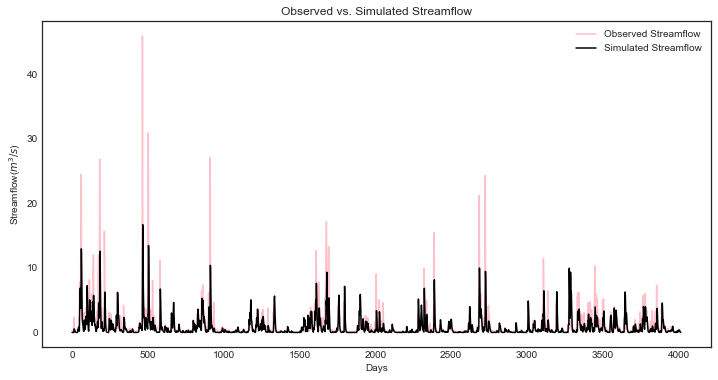

Model outputs include actual evapotranspiration, quick and fast streamflow, and combined runoff. In this tutorial we focus on the total daily runoff, QQ (\(m^3/s\)). We can use the following script to plot simulated streamflow against observed streamflow.

Tip

View the source code used to create this plot here: plot_observed_vs_simulated_streamflow

ax = msdbook.hymod.plot_observed_vs_simulated_streamflow(df=leaf_data, hymod_dict=model)

So how does our model perform? We can investigate model performance across several metrics:

1: Mean Absolute Error (MAE); MAE conveys how the model performs on average across the 10 year simulation period, with smaller values indicating better performance. The absolute value is taken so that positive and negative errors do not cancel each other out.

2: Root Mean Square Error (RMSE); RMSE is sum of square errors across the 10 year simulation period. RMSE is sensitive to large errors between the historical record and the simulated flows, and thus is useful for highlighting the model’s ability to capture of extreme flood events.

3: Log-Root Mean Square Error (Log(RMSE)) LOG(RMSE) focuses on model performance during low-flow events.

mae = np.mean(abs(leaf_data['Strmflw'] - model['Q']))

mse = metrics.mean_squared_error(model['Q'], leaf_data['Strmflw'])

rmse = mse**(1/2)

print('MAE: ' + str(mae) + '\nRMSE: ' + str(mse) + '\nLOG(RMSE): ' + str(rmse))

MAE: 1.0787471470460999

RMSE: 4.375695937555197

LOG(RMSE): 2.0918164206151544

The error metrics show that HYMOD performs reasonably well, the MAE is around 1 \(m^3/s\), the RMSE is on the order of 10% of the largest observed streamflow and the LOG(RMSE) is fairly low.

B.4.3. 2- Global Sensitivity Analysis#

2.1 Experimental Design and Setup

Now we’ll examine how sensitive streamflow simulations generated by HYMOD are to the model’s input parameters. We’ll perform global sensitivity analysis (see Section 3.1 of the main text) using the SALib Python library.

A first and critical step when conducting sensitivity analysis is determining the experimental design (see Design of Experiments, Section 3.4 of the main text). Our experimental design involves defining the uncertainties that we’ll be examining, the output of interest, the ranges of each uncertainty that will be explored and the strategy for sampling the uncertainty space.

For this experiment we’ll explore the five parameters highlighted in Figure 1. We’ll draw their ranges from existing literature on the model (note Jon H. paper). We’ll use a Sobol sampling an a quasi-random sampling with low sequences approach to sample the uncertainty space (Section 3.3.4).

In this demonstration we’ll utilize Sobol Sensitivity Analysis, a variance based method (Section 3.4.5).

To explore HYMOD’s behavoir, we’ll examine the sensitivity of four model ouputs to input parameters: 1) predicted flow, 2) Mean Absolute Error (compared with the calibaration data set), 3) Root Mean Square Error and 1) Log Root Mean Square Error.

This analysis will employ SALib, a Python implementation also utilized in the other SA tutorial (make this more formal).

To start our analysis, we’ll create a dictionary that describes our model uncertainties and their ranges, this dictionary is named “problem_hymod” (SALib refers to these dictionaries as “problems”).

problem_hymod = {

'num_vars': 5,

'names': ['Kq', 'Ks', 'Alp', 'Huz', 'B'],

'bounds': [[0.1, 1], # Kq

[0, 0.1], # Ks

[0, 1], # Alp

[0.1, 500], # Huz

[0, 1.9]] # B

}

After defining our uncertainties and ranges, we’ll use SALib to sample

the uncertainty space and run the model for each of the sample sets. We

will load a sample that has already been created param_values_hymod

for demonstration purposes. For HYMOD, literature recommends running at

least N = 10,000 samples, to keep this demonstration easy to run

however, we utilize only 256 sobol samples of uncertainties. To generate

accurate approximations of second order sensitivity indices SALib

generates N*(2k+2) sets of samples, where N=256 and k=5 (number of

uncertainties). For the math behind why this is needed, see (Saltelli,

A., 2002. Making best use of model evaluations to compute sensitivity

indices. Computer Physics Communications 145, 280–297.

https://doi.org/10.1016/S0010-4655(02)00280-1).

The actual model simulation takes an extended period, so we also load the simulation data from a previous run. The following demonstrates how to conduct this analysis:

# generate 256 samples.

param_values_hymod = saltelli.sample(problem_hymod, 256)

# dictionary to store outputs in

d_outputs = {}

# run simulation for each parameter sample

for i in range(0, len(param_values_hymod)):

# run model for each sensitivity analysis parameter sets

hymod_output = msdbook.hymod(Nq,

param_values_hymod[i, 0],

param_values_hymod[i, 1],

param_values_hymod[i, 2],

param_values_hymod[i, 3],

param_values_hymod[i, 4],

leaf_data,

ndays=4015)

# store the simulated total flow discharge

d_outputs[f"Q{i}"] = hymod_output["Q"]

Q_df_bw = pd.DataFrame(d_outputs)

# load previously generated parameter values

param_values_hymod = load_hymod_params()

# number of samples

n_samples = len(param_values_hymod)

# load previously generated hymod simulated outputs

Q_df_bw = load_hymod_simulation()

# column names of each sample simulation number

sample_column_names = [i for i in Q_df_bw.columns if i[0] == 'Q']

A hydrological model such as HYMOD usually includes ordinary differential equations that are sensitive to their initial condition. They also have components in their underlying formulation that have long memory such that prior time steps can affect their current simulations. For example, soil moisture or groundwater can hold water for a long time and therefore they are often considered to exhibit a long memory. This can affect the partitioning of water to runoff and infiltration, while also controlling the generation of base flow. Therefore, it is important to have a reasonable initial value for them. To achieve this, hydrologists usually extend their simulation period and after the simulations, they remove that extended time period that has unreasonable groundwater or surface water values. This time period is called the warm-up time period.

Here we extended our simulation for one year (from 10 years to 11 years) and we removed the first year of simulation, therefore our warm-up period is one year.

# exclude the first year of simulation from the simulations and reset the index

Q_df = Q_df_bw.iloc[365:4015].copy().reset_index(drop=True)

# exclude the first year of the input data and reset the index

leaf_data = leaf_data.iloc[365:4015].copy().reset_index(drop=True)

Now that HYMOD has been warmed up, we’ll examine how HYMOD’s streamflow outputs vary under different sample sets, and compare them with the observed streamflow.

# add date columns to our simulation data frame; for this data our start date is 1/1/2000

date_ts = pd.date_range(start='1/1/2000', periods=3650, freq='D')

Q_df['date'] = date_ts

Q_df['year'] = date_ts.year

Q_df['month'] = date_ts.month

Q_df['day'] = date_ts.day

# aggregate the simulated observed streamflow to monthly mean

df_sim_mth_mean = Q_df.groupby(['year', 'month'])[sample_column_names].mean()

# do the same for the observed data

date_ts = pd.date_range(start='1/1/2000', periods=len(leaf_data), freq='D')

leaf_data['date'] = date_ts

leaf_data['year'] = date_ts.year

leaf_data['month'] = date_ts.month

leaf_data['day'] = date_ts.day

# aggregate the daily observed streamflow to monthly mean

df_obs_mth_mean = leaf_data.groupby(['year', 'month']).mean()

Tip

View the source code used to create this plot here: plot_observed_vs_sensitivity_streamflow

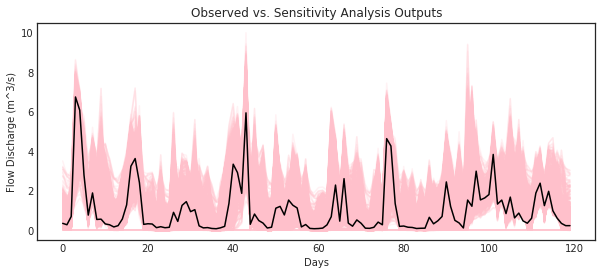

ax = msdbook.hymod.plot_observed_vs_sensitivity_streamflow(df_obs=df_obs_mth_mean,

df_sim=df_sim_mth_mean)

2.2 Sensitivity of streamflows to model parameters

Now we’ll examine how each of HYMOD’s parameters impact the variance of simulated streamflows. Using SALib we’ll calculate the first order and total order sensitivity indices of each model parameter. The first order sensitivity index measure’s the individual impact that a given parameter has on the variance of the simulated streamflows. The total order index measures the impact of a given parameter along with all interactions that other parameters have with the given parameter on simulated streamflows.

We’ll start with an matrix, Y, which contains our simulated streamflows for every uncertainty sample. We’ll then use the sobol.analyze function from SALib to calculate the sensitivity indices (Si). The arguments for this function are the problem dictionary defined in part 2.2 of this tutorial, and the matrix of simulated streamflows, Y.

# overall aggregated indices

Y = Q_df[sample_column_names].mean().to_numpy()

# Perform analysis

Si = sobol.analyze(problem_hymod, Y)

Now we can examine our results, we’ll print the first order and total order Si’s for each parameter, then visualize the results with bar plots

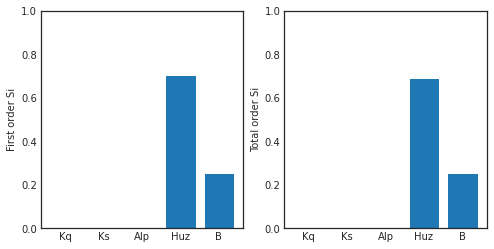

print('First order indices = ', Si['S1'])

print('Total order indices = ', Si['ST'])

sns.set_style('white')

fig = plt.figure(figsize=(8,4))

ax1 = fig.add_subplot(121)

ax1.bar(np.arange(5), Si['S1'])

ax1.set_xticklabels(['','Kq', 'Ks', 'Alp', 'Huz', 'B'])

ax1.set_ylabel('First order Si')

ax1.set_ylim([0,1])

ax2 = fig.add_subplot(122)

ax2.bar(np.arange(5), Si['ST'])

ax2.set_xticklabels(['','Kq', 'Ks', 'Alp', 'Huz', 'B'])

ax2.set_ylabel('Total order Si')

ax2.set_ylim([0,1])

First order indices = [9.55550001e-05 7.49249463e-04 5.62386413e-04 7.03327551e-01

2.53701895e-01]

Total order indicies = [1.76174200e-06 1.63288175e-03 3.41378460e-04 6.88983864e-01

2.53922146e-01]

(0.0, 1.0)

Our findings indicate that in this instance, the streamflow estimate from HYMOD is highly sensitive to soil moisture parameters Huz and B and hardly affected by the routing parameters. Notably, there are very little interactions between parameters causing the total order indices to be nearly identical to the first order indices.

2.3 How do different performance metrics affect the results of our sensitivity analysis?

Streamflow has many different properties. In this section, we discuss how the selection of metrics can lead to fundamentally different sensitivity analysis results. For example, one can only focus on aggregated streamflow metrics such as mean (what has been presented so far), or only on extreme events such as drought or floods.

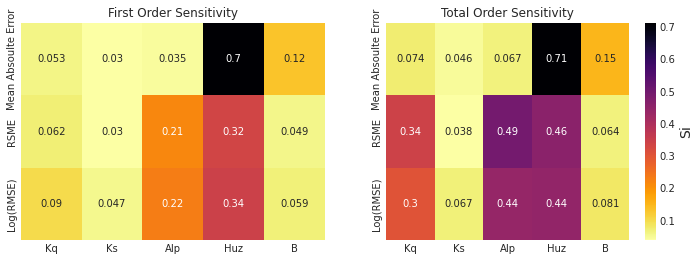

Here we compare three different metrics: 1- Mean error (ME) 2- Root Mean Square Error (RMSE) 3- Log-Root Mean Square Error (Log(RMSE))

Each of these metrics focuses on a specific attribute of streamflow. For example, RMSE highlights the impacts of extreme flood events, while LOG(RMSE) focuses on model performance during low-flow events.

# calculate error metrics

mae = Q_df[sample_column_names].apply(lambda x: abs(x-leaf_data["Strmflw"]), axis=0)

mse = Q_df[sample_column_names].apply(lambda x: metrics.mean_squared_error(x, leaf_data["Strmflw"]), axis=0)

rmse = mse**(1/2)

# add error metrics to a dictionary

d_metrics = {'MAE': mae.mean().values,

'RMSE': rmse.values,

'LOG[RMSE]': np.log10(rmse.values)}

# convert to a dataframe

df_metrics_SA = pd.DataFrame(d_metrics)

We can use the following to calculate the SA indices for each metric and visualize it.

df_metric_s1_result = pd.DataFrame(np.zeros((3, 5)), columns=['Kq', 'Ks', 'Alp', 'Huz', 'B'])

df_metric_sT_result = pd.DataFrame(np.zeros((3, 5)), columns=['Kq', 'Ks', 'Alp', 'Huz', 'B'])

# conduct sensitivity analysis for each metric

for index, i in enumerate(d_metrics.keys()):

# get the data as a numpy array for the target metric

Y = d_metrics[i]

# use the metric to conduct SA

Si = sobol.analyze(problem_hymod, Y, print_to_console=False)

# add the sensitivity indices to the output data frame

df_metric_s1_result.iloc[index, :] = Si['S1']

df_metric_sT_result.iloc[index, :] = Si['ST']

# create seaborn heatmap with required labels

fig = plt.figure(figsize=(12,4))

ax1 = fig.add_subplot(121)

# labels for y-axis

y_axis_labels = ['Mean Absolute Error', 'RSME', 'Log(RMSE)']

# plot heatmap

ax1 = sns.heatmap(df_metric_s1_result, yticklabels=y_axis_labels, annot=True, cmap='inferno_r', cbar_kws={'label': 'Si'}, cbar=False)

ax1.figure.axes[-1].yaxis.label.set_size(14)

ax1.set_title('First Order Sensitivity')

ax2 = fig.add_subplot(122)

ax2 = sns.heatmap(df_metric_sT_result, yticklabels=y_axis_labels, annot=True, cmap='inferno_r', cbar_kws={'label': 'Si'})

ax2.figure.axes[-1].yaxis.label.set_size(14)

ax2.set_title('Total Order Sensitivity')

Text(0.5, 1.0, 'Total Order Sensitivity')

The first order sensitivity indices indicate that HYMOD’s sensitivity to its parameters is different depending on how its output is measured. Unsurprisingly, the mean absolute error is highly sensitive to the soil moisture accounting parameters Huz and B, just like the overall streamflow predictions above. However, when we examine RMSE and log(RMSE), the routing parameters Alp become sensitive, and the sensitivity to parameter B is reduced. As described above, RMSE and LOG(RMSE) respond to model performance in high-flow and low flow periods respectively. Our results indicate that for these flow regimes Alp, the parameter that governs the split between quick and slow flow is an important factor. While still the parameter with the highest most effect on all three measures, Huz is much less influential for RMSE and LOG(RMSE) than it is for MAE.

The total order sensitivity indices review a different, more complex story. While the MAE sensitivity is relatively governed by first order effects (like the streamflow predictions above), the RMSE and LOG(RMSE) error metrics show significant interactions. Alp has the highest total order sensitivity for RMSE and is equal to Huz for Log(RMSE). Kq, which has a relatively low first order sensitivity index, shows strong contribution to variance when interactions are taken into account.

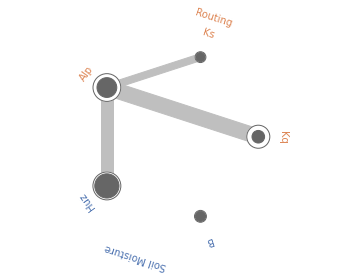

Radial convergence plots are a helpful way to visualize the interactions between parameters. These plots array the model parameters in a circle and plot the first order, total order and second order Sobol sensitivity indices for each parameter. The first order sensitivity is shown as the size of a closed circle, the total order as the size of a larger open circle and the second order as the thickness of a line connecting two parameters. Below is an example of a radial convergence plot for the LOG(RMSE) measure. The plot indicates strong interactions between the Huz and Alp parameters, as well as Alp and Kq. There is also an interaction between Alp and Ks.

sns.set_style('whitegrid', {'axes_linewidth': 0, 'axes.edgecolor': 'white'})

def is_significant(value, confidence_interval, threshold="conf"):

if threshold == "conf":

return value - abs(confidence_interval) > 0

else:

return value - abs(float(threshold)) > 0

def grouped_radial(SAresults, parameters, radSc=2.0, scaling=1, widthSc=0.5, STthick=1, varNameMult=1.3, colors=None, groups=None, gpNameMult=1.5, threshold="conf"):

# Derived from https://github.com/calvinwhealton/SensitivityAnalysisPlots

fig, ax = plt.subplots(1, 1)

color_map = {}

# initialize parameters and colors

if groups is None:

if colors is None:

colors = ["k"]

for i, parameter in enumerate(parameters):

color_map[parameter] = colors[i % len(colors)]

else:

if colors is None:

colors = sns.color_palette("deep", max(3, len(groups)))

for i, key in enumerate(groups.keys()):

for parameter in groups[key]:

color_map[parameter] = colors[i % len(colors)]

n = len(parameters)

angles = radSc*math.pi*np.arange(0, n)/n

x = radSc*np.cos(angles)

y = radSc*np.sin(angles)

# plot second-order indices

for i, j in itertools.combinations(range(n), 2):

if is_significant(SAresults["S2"][i][j], SAresults["S2_conf"][i][j], threshold):

angle = math.atan((y[j]-y[i])/(x[j]-x[i]))

if y[j]-y[i] < 0:

angle += math.pi

line_hw = scaling*(max(0, SAresults["S2"][i][j])**widthSc)/2

coords = np.empty((4, 2))

coords[0, 0] = x[i] - line_hw*math.sin(angle)

coords[1, 0] = x[i] + line_hw*math.sin(angle)

coords[2, 0] = x[j] + line_hw*math.sin(angle)

coords[3, 0] = x[j] - line_hw*math.sin(angle)

coords[0, 1] = y[i] + line_hw*math.cos(angle)

coords[1, 1] = y[i] - line_hw*math.cos(angle)

coords[2, 1] = y[j] - line_hw*math.cos(angle)

coords[3, 1] = y[j] + line_hw*math.cos(angle)

ax.add_artist(plt.Polygon(coords, color="0.75"))

# plot total order indices

for i, key in enumerate(parameters):

if is_significant(SAresults["ST"][i], SAresults["ST_conf"][i], threshold):

ax.add_artist(plt.Circle((x[i], y[i]), scaling*(SAresults["ST"][i]**widthSc)/2, color='w'))

ax.add_artist(plt.Circle((x[i], y[i]), scaling*(SAresults["ST"][i]**widthSc)/2, lw=STthick, color='0.4', fill=False))

# plot first-order indices

for i, key in enumerate(parameters):

if is_significant(SAresults["S1"][i], SAresults["S1_conf"][i], threshold):

ax.add_artist(plt.Circle((x[i], y[i]), scaling*(SAresults["S1"][i]**widthSc)/2, color='0.4'))

# add labels

for i, key in enumerate(parameters):

ax.text(varNameMult*x[i], varNameMult*y[i], key, ha='center', va='center',

rotation=angles[i]*360/(2*math.pi) - 90,

color=color_map[key])

if groups is not None:

for i, group in enumerate(groups.keys()):

print(group)

group_angle = np.mean([angles[j] for j in range(n) if parameters[j] in groups[group]])

ax.text(gpNameMult*radSc*math.cos(group_angle), gpNameMult*radSc*math.sin(group_angle), group, ha='center', va='center',

rotation=group_angle*360/(2*math.pi) - 90,

color=colors[i % len(colors)])

ax.set_facecolor('white')

ax.set_xticks([])

ax.set_yticks([])

plt.axis('equal')

plt.axis([-2*radSc, 2*radSc, -2*radSc, 2*radSc])

return fig

# define groups for parameter uncertainties

groups={"Soil Moisture" : ["Huz", "B"],

"Routing" : ["Alp", "Kq", "Ks"]}

fig = grouped_radial(Si, ['Kq', 'Ks', 'Alp', 'Huz', 'B'], groups=groups, threshold=0.025)

Soil Moisture

Routing

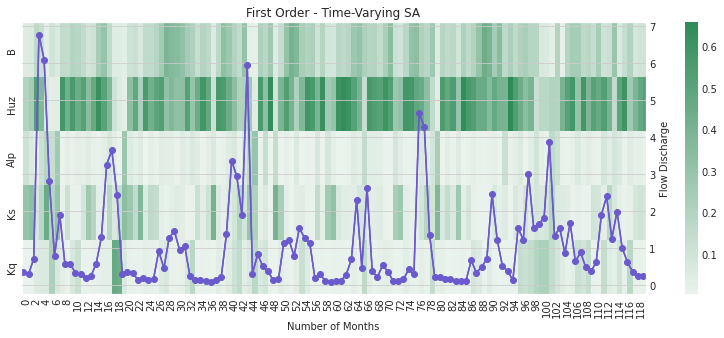

2.4 Time-Varying Sensitivity Analysis

In section 2.5 we saw how performing sensitivity analysis on different measurements of model output can yield in different results on the importance of each uncertain input. In this section we’ll examine how performing this analysis over time can yield additional insight into the performance of HYMOD. We’ll first examine how model sensitivities vary by month, then examine how they change across each year of the simulation.

For this demonstration, we’ll focus only on the monthly streamflow predictions generated by HYMOD.

# aggregate simulated streamflow data to monthly time series

df_sim_by_mth_mean = Q_df.groupby('month')[sample_column_names].mean()

# aggregate observed streamflow data to monthly time series

df_obs_by_mth_mean = leaf_data.groupby('month').mean()

We can use the following to calculate the SA indices for each month and visualize it. Results are pre-loaded for efficiency.

# set up dataframes to store outputs

df_mth_s1 = pd.DataFrame(np.zeros((12,5)), columns=['Kq', 'Ks', 'Alp', 'Huz', 'B'])

df_mth_delta = df_mth_s1.copy()

# iterate through each month

for i in range(0, 12):

# generate the simulation data

Y = df_sim_by_mth_mean.iloc[i, :].to_numpy()

# run SA

Si = delta.analyze(problem_hymod, param_values_hymod, Y, print_to_console=False)

# add to output dataframes

df_mth_s1.iloc[i, :] = np.maximum(Si['S1'], 0)

df_mth_delta.iloc[i, :] = np.maximum(Si['delta'], 0)

# convert to arrays

arr_mth_s1 = df_mth_s1.values

arr_mth_delta = df_mth_delta.values

The following can be used to visualize the time-varying first-order indices. The first order represents the direct impacts of a specific parameter on model outputs.

Tip

View the source code used to create this plot here: plot_monthly_heatmap

# load previously ran data

arr_mth_delta, arr_mth_s1 = msdbook.load_hymod_monthly_simulations()

# plot figure

ax, ax2 = msdbook.hymod.plot_monthly_heatmap(arr_sim=arr_mth_s1.T,

df_obs=df_obs_by_mth_mean,

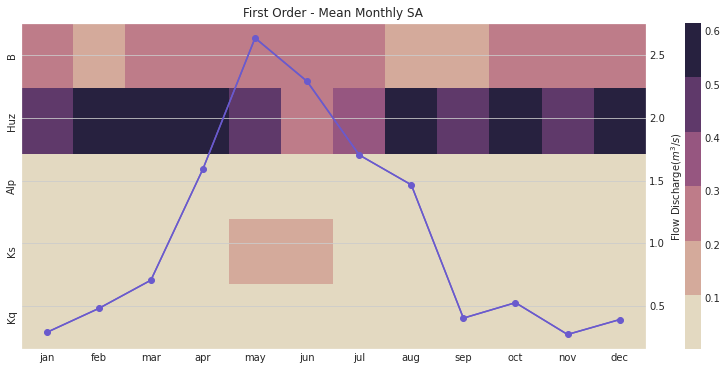

title='First Order - Mean Monthly SA')

This figure demonstrates the first order sensitivity indices when the streamflow data are aggregated by month. The purple line represents the observed monthly discharge. The figure indicates that the first order indices are highest for B and Huz across all months and lowest for Alp, Ks, and Kq. Note that in the months with the highest flow, Ks becomes an influential parameter.

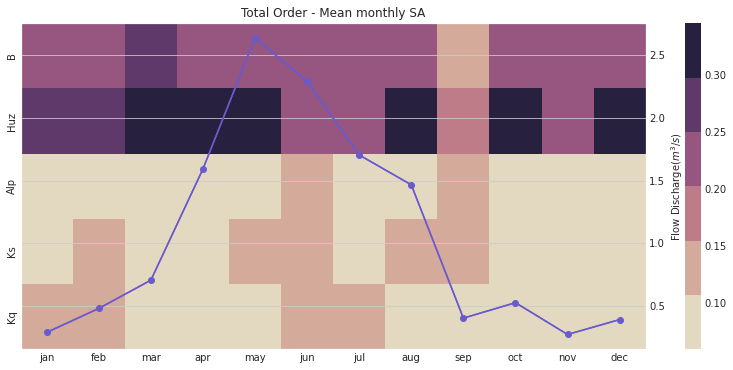

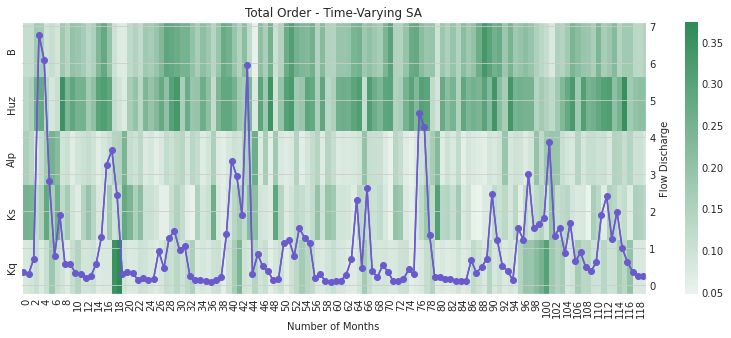

We can also focus on the total order sensitivity index that includes first-order SA indices and interactions between parameters

# plot figure

ax, ax2 = msdbook.hymod.plot_monthly_heatmap(arr_sim=arr_mth_delta.T,

df_obs=df_obs_by_mth_mean,

title='Total Order - Mean monthly SA')

Notably, the total order sensitivity results are different than the first order sensitivity results, which indicates that interactions between the parameters (particularly in regards to routing parameters \(Kq\), \(Ks\), and \(Alp\)) contribute to changes in HYMOD output.

# group by year and get mean

df_sim_by_yr_mean = Q_df.groupby(['year'])[sample_column_names].mean()

# group input data and get mean

df_obs_by_yr_mean = leaf_data.groupby(['year']).mean()

We can also calculate the sensitivity analysis indices for each individual year. This will allow us to understand if model control changes during different years. The following code first aggregates the outputs to annual time steps, and then calculates the SA indices.

# set up dataframes to store outputs

df_yr_s1 = pd.DataFrame(np.zeros((10, 5)), columns=['Kq', 'Ks', 'Alp', 'Huz', 'B'])

df_yr_delta = df_yr_s1.copy()

# iterate through each year

for i in range(0, 10):

# generate the simulation data

Y = df_sim_by_yr_mean.iloc[i, :].to_numpy()

# run SA

Si = delta.analyze(problem_hymod, param_values_hymod, Y, print_to_console=False)

# add to output dataframes

df_yr_s1.iloc[i, :] = np.maximum(Si['S1'], 0)

df_yr_delta.iloc[i, :] = np.maximum(Si['delta'], 0)

# convert to arrays

arr_yr_s1 = df_mth_s1.values

arr_yr_delta = df_mth_delta.values

Tip

View the source code used to create this plot here: plot_annual_heatmap

# load previously ran data

arr_yr_delta, arr_yr_s1 = load_hymod_annual_simulations()

# plot figure

ax, ax2 = msdbook.hymod.plot_annual_heatmap(arr_sim=arr_yr_s1.T,

df_obs=df_obs_by_yr_mean,

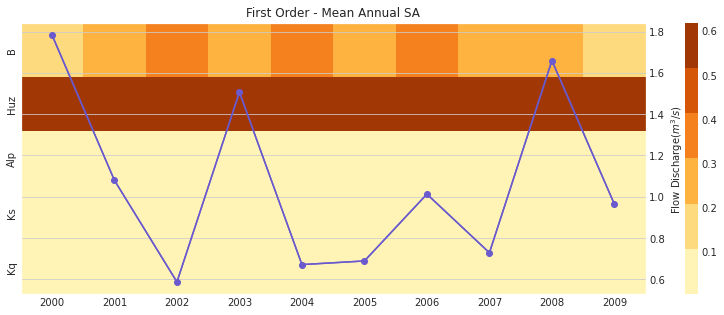

title='First Order - Mean Annual SA')

The first order sensitivities at the annual scale are not unlike the first order monthly sensitivities. Once again, sensitivities vary across year and Huz and B are the most consequential parameters.

# plot figure

ax, ax2 = msdbook.hymod.plot_annual_heatmap(arr_sim=arr_yr_delta.T,

df_obs=df_obs_by_yr_mean,

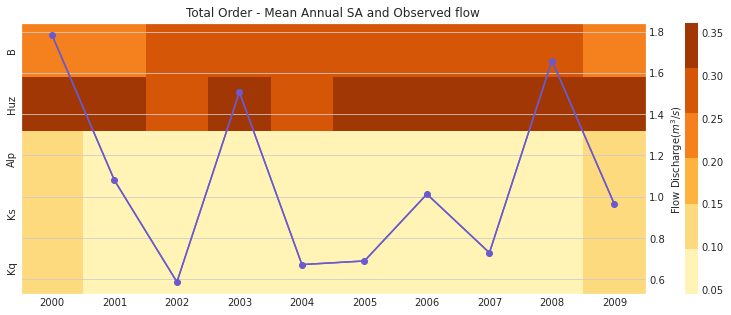

title='Total Order - Mean Annual SA and Observed flow')

Our results indicate that sensitivity analysis indices vary in different years and now that interactions are included, the Kq, Ks, and Alp variables impact the sensitivity of the streamflow output.